FATF Travel Rule 2025: US Crypto Compliance & Avoiding Penalties

The cryptocurrency landscape is constantly evolving, and with its growth comes increased scrutiny from global regulatory bodies. One of the most significant developments impacting Virtual Asset Service Providers (VASPs) worldwide, and particularly in the United States, is the Financial Action Task Force (FATF) Travel Rule. As we approach 2025, the implications of this rule are becoming clearer, and US crypto businesses must take proactive steps to ensure compliance and avoid severe penalties.

This comprehensive guide delves into the intricacies of the FATF Travel Rule, its impending impact on US crypto operations, and practical, actionable strategies for achieving compliance. Understanding and implementing these measures is not just about avoiding fines; it’s about safeguarding your business’s reputation, fostering trust, and ensuring long-term viability in a regulated financial ecosystem.

What is the FATF Travel Rule? A Deep Dive into its Origins and Purpose

The FATF Travel Rule, formally known as Recommendation 16, is a crucial component of the Financial Action Task Force’s (FATF) anti-money laundering (AML) and counter-terrorist financing (CFT) framework. Established in 1989, the FATF is an intergovernmental organization that sets international standards to prevent these illicit activities. In June 2019, the FATF updated its guidance to explicitly include virtual assets (VAs) and VASPs within the scope of its recommendations, effectively extending traditional financial regulations to the nascent crypto industry.

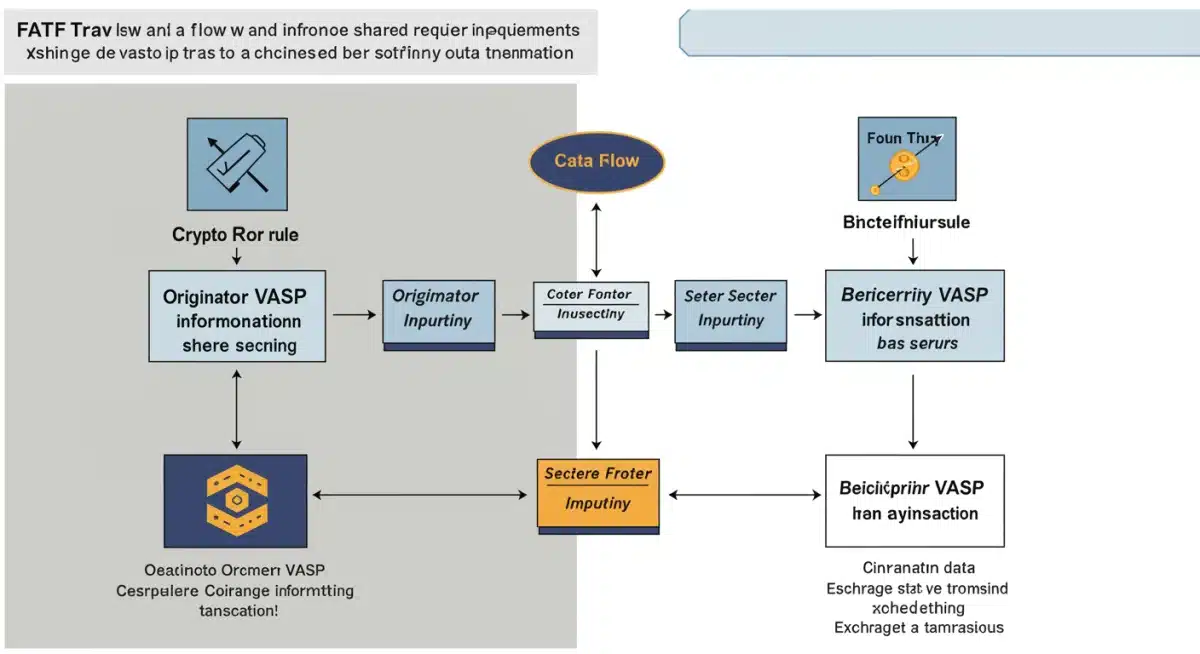

The core principle of the Travel Rule is simple: just as traditional financial institutions (like banks) are required to collect and transmit specific originator and beneficiary information for wire transfers above a certain threshold, VASPs must do the same for virtual asset transfers. This means that when a customer initiates a crypto transaction from one VASP to another, both the sending (originator) and receiving (beneficiary) VASPs must collect, hold, and exchange certain identifying information about their respective customers.

The primary purpose of the FATF Travel Rule is to prevent the use of virtual assets for money laundering, terrorist financing, and other illicit financial activities. By requiring VASPs to share transactional data, regulators aim to create a transparent audit trail for crypto transactions, making it harder for criminals to move funds anonymously. This increased transparency is seen as vital for maintaining the integrity of the global financial system and protecting consumers from fraud and exploitation.

The FATF does not directly enforce the Travel Rule; instead, it sets the standards that its member countries, including the United States, are expected to implement through their national laws and regulations. This means that while the FATF provides the framework, the specific details of how the Travel Rule is implemented can vary slightly from jurisdiction to jurisdiction, leading to a complex and fragmented regulatory landscape for global VASPs.

For US crypto businesses, compliance with the FATF Travel Rule is primarily enforced by the Financial Crimes Enforcement Network (FinCEN), which is responsible for administering the Bank Secrecy Act (BSA) and its implementing regulations. FinCEN has issued guidance clarifying that VASPs are considered money service businesses (MSBs) under US law and are therefore subject to AML/CFT obligations, including those related to the Travel Rule.

The threshold for applying the Travel Rule in the US is currently set at $3,000 for transfers. This means that for any virtual asset transfer equal to or exceeding $3,000, US VASPs must collect and transmit the required information. However, it’s crucial for businesses to stay updated, as regulatory thresholds can change, and global standards often aim for lower thresholds or even zero-threshold applications in the future.

Why 2025 is a Critical Year for US Crypto Businesses

While the FATF Travel Rule was introduced in 2019, 2025 is shaping up to be a pivotal year for its enforcement and widespread adoption, particularly within the US crypto ecosystem. Several factors contribute to this heightened urgency:

Increasing Regulatory Pressure and Scrutiny

Global regulatory bodies, including the FATF, FinCEN, and other national authorities, have consistently emphasized the need for comprehensive implementation of the Travel Rule. The grace period for adoption is drawing to a close, and regulators are signaling a move towards stricter enforcement. This means that businesses that have been slow to adapt will face increased scrutiny and a higher likelihood of penalties.

Technological Solutions Reaching Maturity

One of the initial challenges of the Travel Rule was the lack of interoperable technical solutions for VASPs to share information securely and efficiently. However, in recent years, various industry-led working groups and technology providers have developed robust protocols and platforms (e.g., TRISA, Shyft Network, Travel Rule Universal Protocol – TRUP) designed to facilitate Travel Rule compliance. The maturity of these solutions removes a significant barrier to implementation, making non-compliance less excusable.

Global Harmonization Efforts

As more jurisdictions implement the Travel Rule, there’s a growing push for greater harmonization of standards and technical approaches. This means that US VASPs will increasingly need to be able to interact with compliant VASPs in other countries, necessitating their own robust compliance frameworks. Non-compliance could lead to isolation from global crypto markets.

Growing Enforcement Actions

Regulators are not just issuing warnings; they are taking action. We’ve seen a rise in enforcement actions against crypto businesses that fail to meet AML/CFT obligations, including those related to the Travel Rule. These actions serve as a stark reminder of the financial and reputational risks associated with non-compliance.

The Evolving Threat Landscape

The use of virtual assets by illicit actors continues to evolve. Regulators are keen to close any loopholes that allow criminals to exploit the crypto ecosystem. The Travel Rule is a critical tool in this fight, and its full implementation is seen as essential to mitigating these evolving threats.

For US crypto businesses, 2025 represents a critical juncture. It’s the year when comprehensive FATF Travel Rule compliance will no longer be an aspiration but a fundamental requirement for operating legitimately within the virtual asset space. Proactive preparation is paramount to navigate this regulatory shift successfully.

The Information Exchange Mandate: What Data Needs to Be Shared?

At the heart of the FATF Travel Rule is the requirement for VASPs to collect and transmit specific information about the originator and beneficiary of a virtual asset transfer. This ensures that authorities can trace the flow of funds and identify individuals involved in transactions, just as they would with traditional wire transfers.

Originator Information (Sending VASP’s Responsibility):

- Originator’s Full Name: The complete legal name of the individual or entity sending the virtual assets.

- Originator’s Account Number: The account identifier used by the originator at the sending VASP (e.g., wallet address, internal account ID).

- Originator’s Physical Address: The residential or business address of the sender.

- Originator’s National Identity Number (if available): Such as a Social Security Number (SSN) in the US, or other government-issued ID.

- Originator’s Date and Place of Birth (for individuals): Essential for identity verification.

Beneficiary Information (Receiving VASP’s Responsibility):

- Beneficiary’s Full Name: The complete legal name of the individual or entity receiving the virtual assets.

- Beneficiary’s Account Number: The account identifier used by the beneficiary at the receiving VASP.

It’s important to note that while the sending VASP is generally responsible for collecting and transmitting both originator and beneficiary information to the receiving VASP, the receiving VASP also has obligations. The receiving VASP must ensure that it receives the required information and, if it identifies any missing or inconsistent data, it must take reasonable steps to obtain it or report the transaction as suspicious if concerns persist.

The specific threshold for transmitting this information in the US is currently set at $3,000. This means that for any virtual asset transfer equal to or exceeding $3,000, US VASPs must collect and transmit the required information. For transfers below this threshold, VASPs are generally still required to collect and hold this information, but not necessarily transmit it to the beneficiary VASP, unless deemed suspicious.

The secure transmission of this sensitive personal data is a critical aspect of compliance. VASPs cannot simply send unencrypted emails or use insecure channels. They must employ secure, interoperable solutions that protect customer privacy while facilitating regulatory compliance. This is where the emerging Travel Rule solutions play a vital role, providing encrypted and standardized communication channels between VASPs.

Failure to comply with these information exchange mandates can lead to significant regulatory penalties, including fines, operational restrictions, and reputational damage. Therefore, US crypto businesses must meticulously review their data collection and transmission protocols to ensure they align with FATF and FinCEN requirements.

Practical Steps for US Crypto Businesses to Achieve Compliance

Navigating the complexities of the FATF Travel Rule requires a strategic and multi-faceted approach. US crypto businesses must implement robust compliance frameworks to meet these evolving regulatory demands. Here are practical steps to ensure your business is prepared for 2025:

1. Conduct a Comprehensive Risk Assessment

Begin by understanding your specific exposure. A thorough risk assessment identifies potential vulnerabilities related to money laundering and terrorist financing within your operations. This should include an analysis of your customer base, the types of virtual assets you support, transaction volumes, geographic reach, and existing AML/CFT controls. This assessment will inform the scope and intensity of your Travel Rule compliance program.

2. Update Your AML/CFT Program

Your existing AML/CFT program needs to be revised to explicitly incorporate Travel Rule requirements. This includes:

- Enhanced Customer Due Diligence (CDD): Ensure your KYC (Know Your Customer) processes collect all necessary originator and beneficiary information (full name, address, account numbers, etc.) at onboarding and during ongoing monitoring.

- Transaction Monitoring: Implement systems to identify transactions that meet or exceed the Travel Rule threshold ($3,000 in the US) and flag suspicious activity.

- Record-Keeping: Establish secure and auditable procedures for storing all collected Travel Rule data for the required period (typically five years in the US).

3. Implement a Travel Rule Solution Provider (TRP)

Manually exchanging sensitive data with every counterparty VASP is impractical and insecure. Partnering with a specialized Travel Rule Solution Provider (TRP) is crucial. These providers offer secure, interoperable platforms that facilitate the compliant exchange of Travel Rule data between VASPs. Research and select a TRP that:

- Supports relevant protocols (e.g., TRISA, TRUP).

- Offers robust security and data privacy features.

- Provides comprehensive VASP discovery and verification mechanisms.

- Is widely adopted by other VASPs in your network.

4. Develop Internal Policies and Procedures

Formalize your Travel Rule compliance program with clear, written policies and procedures. These should outline:

- The roles and responsibilities of staff involved in Travel Rule compliance.

- The process for identifying and verifying counterparty VASPs.

- Detailed steps for collecting, transmitting, and receiving required information.

- Protocols for handling missing or incomplete information.

- Procedures for reporting suspicious transactions to FinCEN (e.g., SAR filings).

- Data retention and privacy safeguards.

5. Train Your Staff

Even the best policies are ineffective without proper training. All relevant employees, from customer service to compliance officers and technical staff, must be thoroughly trained on the FATF Travel Rule, your company’s specific procedures, and the use of any compliance technology. Regular refresher training is also essential to keep staff up-to-date with evolving regulations and internal processes.

6. Establish VASP Due Diligence Protocols

Before engaging in transactions with another VASP, you must perform due diligence to ensure they are also compliant with the Travel Rule. This involves verifying their identity, regulatory status, and their ability to receive and transmit the required information securely. Many TRPs offer tools to assist with VASP discovery and verification.

7. Monitor and Audit Your Compliance Program Regularly

Compliance is not a one-time event. Continuously monitor your Travel Rule compliance program for effectiveness. Conduct regular internal audits to identify any gaps or weaknesses. Be prepared for external audits by regulators and ensure all documentation and records are readily accessible. This proactive approach allows for continuous improvement and demonstrates a commitment to compliance.

8. Stay Informed and Adapt

The regulatory landscape for virtual assets is dynamic. Stay abreast of new guidance from FATF, FinCEN, and other relevant authorities. Engage with industry associations and legal counsel to ensure your compliance program remains current and adaptable to future changes. This includes monitoring for potential changes in thresholds or reporting requirements.

By systematically addressing these steps, US crypto businesses can build a robust FATF Travel Rule compliance framework, mitigate regulatory risks, and securely operate within the evolving virtual asset ecosystem.

The Consequences of Non-Compliance: Penalties and Reputational Damage

Ignoring the FATF Travel Rule in 2025 is not an option for US crypto businesses. The consequences of non-compliance can be severe, impacting a company’s financial health, operational capabilities, and public trust. Understanding these risks underscores the urgency of implementing a robust compliance program.

Significant Financial Penalties

FinCEN, the primary enforcer of AML/CFT regulations in the US, has the authority to impose substantial fines for violations of the Bank Secrecy Act (BSA), which includes Travel Rule requirements. These penalties can range from thousands to millions of dollars, depending on the severity and frequency of the violations. For instance, a single transaction that fails to meet Travel Rule requirements could result in a fine, and repeated or systemic failures can lead to escalating penalties that could cripple a business.

Beyond direct fines, non-compliance can lead to other financial repercussions, such as asset forfeitures if illicit funds are found to have passed through a non-compliant platform.

Operational Restrictions and Suspension of Services

Regulators can impose operational restrictions on non-compliant businesses. This might include limiting the types of services offered, restricting transaction volumes, or even suspending operations entirely. Such measures can effectively shut down a business, preventing it from serving its customers or engaging in virtual asset transfers. In extreme cases, licenses to operate as a Money Services Business (MSB) could be revoked.

Reputational Damage and Loss of Trust

In the financial sector, trust is paramount. A public enforcement action for AML/CFT or Travel Rule violations can severely damage a crypto business’s reputation. News of non-compliance can erode customer trust, lead to a loss of existing clients, and deter potential new users. It can also make it difficult to secure partnerships with other compliant VASPs, traditional financial institutions, or investors, effectively isolating the business within the ecosystem. Rebuilding a damaged reputation is a long and arduous process, often more costly than initial compliance efforts.

Legal Liability and Criminal Charges

Individuals within a crypto business, particularly compliance officers and senior management, can face personal legal liability for significant and willful AML/CFT violations. In severe cases, this could lead to criminal charges, including imprisonment, especially if there’s evidence of aiding and abetting money laundering or terrorist financing activities.

Increased Scrutiny from Other Regulators

A violation of the Travel Rule or other AML/CFT requirements can trigger increased scrutiny from other regulatory bodies, both domestically and internationally. This can lead to broader investigations into a company’s operations, potentially uncovering other areas of non-compliance and further escalating penalties.

Exclusion from the Global Financial System

As the FATF Travel Rule becomes a global standard, non-compliant VASPs risk being cut off from the broader financial ecosystem. Compliant VASPs will be hesitant to interact with non-compliant entities to avoid their own regulatory risks. This could severely limit a business’s ability to conduct international transactions or engage with a wide range of partners, hindering growth and market access.

The message is clear: proactive and thorough compliance with the FATF Travel Rule is not merely a suggestion but a fundamental requirement for the continued operation and success of any US crypto business. The costs of compliance, while potentially significant, are far outweighed by the punitive consequences of non-compliance.

The Future of Crypto Regulation: Beyond the Travel Rule

While the FATF Travel Rule is a dominant force shaping crypto compliance in 2025, it’s crucial for US crypto businesses to understand that the regulatory landscape is continuously evolving. The Travel Rule is just one piece of a broader puzzle aimed at integrating virtual assets into the regulated financial system. Looking ahead, several other regulatory trends and developments are likely to impact the industry:

Enhanced DeFi Scrutiny

Decentralized Finance (DeFi) has largely operated in a regulatory grey area. However, regulators globally, including FinCEN and the FATF, are increasingly scrutinizing DeFi protocols, particularly those that exhibit characteristics similar to traditional financial services. Expect to see efforts to define and regulate entities within the DeFi space, potentially extending AML/CFT obligations to developers, front-end operators, or even liquidity providers. The challenge here is applying traditional regulatory frameworks to truly decentralized systems, but the intent to bring DeFi under supervision is clear.

Stablecoin Regulation

The stability and widespread adoption of stablecoins have drawn significant attention from central banks and financial regulators. Concerns about monetary stability, consumer protection, and systemic risk are driving calls for comprehensive stablecoin regulation. In the US, proposals like the stablecoin reserve requirements and licensing frameworks are being discussed. This could lead to stablecoin issuers being treated more like banks or money market funds, with stringent capital, liquidity, and operational requirements.

NFTs and Digital Collectibles

Initially often viewed as unique digital art, the increasing financialization of Non-Fungible Tokens (NFTs) and other digital collectibles is attracting regulatory interest. When NFTs are used for investment purposes, fractionalized, or serve as collateral for loans, they begin to resemble traditional securities or financial instruments. Regulators may move to classify certain NFTs as securities, subjecting platforms facilitating their trade to securities laws, including KYC/AML requirements.

Global Regulatory Cooperation and Data Sharing

The cross-border nature of cryptocurrency necessitates international cooperation. Beyond the Travel Rule, expect increased collaboration among global regulators to harmonize standards, share intelligence, and coordinate enforcement actions. This could lead to more standardized reporting requirements and a more interconnected regulatory framework, making it harder for illicit actors to exploit jurisdictional arbitrage.

Cybersecurity and Data Privacy

As more sensitive customer data is collected and exchanged under regulations like the Travel Rule, cybersecurity and data privacy become even more critical. Regulators will likely enforce stricter standards for data protection, encryption, and breach notification. US crypto businesses must invest heavily in robust cybersecurity infrastructure and adhere to global data privacy laws like GDPR (for international operations) and state-specific privacy laws.

Environmental, Social, and Governance (ESG) Concerns

The environmental impact of proof-of-work cryptocurrencies has become a significant concern. While not directly a financial regulation, ESG considerations could indirectly influence regulatory policy, investment decisions, and public perception, potentially favoring more energy-efficient blockchain technologies or requiring disclosures of environmental impact.

For US crypto businesses, the key takeaway is that compliance with the FATF Travel Rule is a foundational step, but not the final destination. A forward-looking strategy involves anticipating these broader regulatory trends, building adaptable compliance systems, and maintaining an open dialogue with regulators. Proactive engagement and a commitment to responsible innovation will be crucial for long-term success in this dynamic environment.

Conclusion: Embracing Compliance for a Sustainable Future

The FATF Travel Rule, with its critical implementation phase in 2025, represents a significant turning point for US crypto businesses. It marks a clear intention by global and national regulators to bring the virtual asset ecosystem into alignment with traditional financial anti-money laundering and counter-terrorist financing standards. For businesses operating in this space, ignoring these mandates is not merely a risk; it is a direct threat to their very existence.

Embracing compliance with the FATF Travel Rule is more than just avoiding penalties; it is about establishing a foundation of trust, legitimacy, and sustainability. A compliant business is a secure business, one that protects its users from illicit activities and safeguards its own reputation in a rapidly maturing industry. It demonstrates a commitment to ethical operations and positions itself as a responsible participant in the global financial landscape.

The practical steps outlined in this guide – from comprehensive risk assessments and updated AML/CFT programs to the implementation of robust Travel Rule solutions, thorough staff training, and continuous monitoring – are not merely checkboxes to tick. They are integral components of a strategic framework designed to navigate the complexities of modern financial regulation. By investing in these areas, US crypto businesses can transform regulatory challenges into opportunities for growth, fostering stronger relationships with customers, partners, and regulators alike.

As the crypto industry continues its trajectory of innovation, regulatory frameworks will undoubtedly evolve further. The Travel Rule serves as a powerful reminder that proactive engagement with these changes, rather than reactive adaptation, is the hallmark of resilient and successful enterprises. By prioritizing compliance now, US crypto businesses can ensure their place in a future where virtual assets are not only technologically advanced but also seamlessly integrated into a secure and regulated global financial system. The time to act is now, setting the stage for a secure and prosperous future in the world of decentralized finance.