FinCEN Reporting Deadlines 2026: Crypto Businesses Must Prepare Now

The regulatory landscape for virtual assets in the United States is constantly evolving, with the Financial Crimes Enforcement Network (FinCEN) playing a pivotal role in ensuring the integrity of the financial system. For US crypto businesses, a critical period is fast approaching: the Q3 2026 FinCEN reporting deadlines. These deadlines are not merely administrative hurdles; they represent a significant step in the broader effort to combat money laundering, terrorist financing, and other illicit activities within the burgeoning digital asset ecosystem. Ignoring these requirements can lead to severe penalties, reputational damage, and operational disruptions. Therefore, proactive preparation is not just advisable; it’s imperative.

This comprehensive guide delves into the intricacies of FinCEN Crypto Reporting, outlining what US crypto businesses need to know and, more importantly, what they need to do to ensure full compliance by Q3 2026. We will explore the regulatory framework, identify key reporting obligations, discuss the challenges unique to virtual assets, and provide actionable strategies for effective preparation. Our aim is to equip you with the knowledge and tools necessary to navigate this complex terrain successfully, safeguarding your business against potential pitfalls and fostering a culture of robust compliance.

Understanding FinCEN’s Mandate and the Evolution of Crypto Regulation

FinCEN, a bureau of the U.S. Department of the Treasury, serves as the primary agency responsible for administering the Bank Secrecy Act (BSA). Its mission is to safeguard the financial system from illicit use, combat money laundering, and promote national security through the strategic use of financial authorities and the collection, analysis, and dissemination of financial intelligence. With the rise of cryptocurrencies and other virtual assets, FinCEN’s purview has naturally expanded to encompass this innovative, yet often opaque, sector.

The journey of regulating virtual assets has been a dynamic one. Initially, many thought of cryptocurrencies as a niche technological curiosity. However, their rapid adoption, increasing market capitalization, and potential for facilitating both legitimate and illicit transactions quickly brought them under the scrutiny of financial regulators worldwide. FinCEN was among the first to clarify its stance, issuing guidance as early as 2013, stating that administrators and exchangers of virtual currency are considered money transmitters under the BSA and are thus subject to its regulations.

Subsequent guidance and enforcement actions have further solidified FinCEN’s position, clarifying that various entities involved in virtual asset activities, including exchanges, certain wallet providers, and even some decentralized finance (DeFi) platforms, may fall under the definition of Money Services Businesses (MSBs). This classification brings with it a host of obligations, including anti-money laundering (AML) program requirements, recordkeeping, and, crucially, reporting obligations.

The Q3 2026 FinCEN reporting deadlines are a culmination of these ongoing regulatory efforts, signaling a mature phase where compliance expectations are clearly defined and enforced. Businesses operating in the crypto space can no longer afford to operate in a regulatory gray area; clear understanding and adherence to these guidelines are paramount for long-term viability and success.

Key FinCEN Reporting Obligations for Crypto Businesses

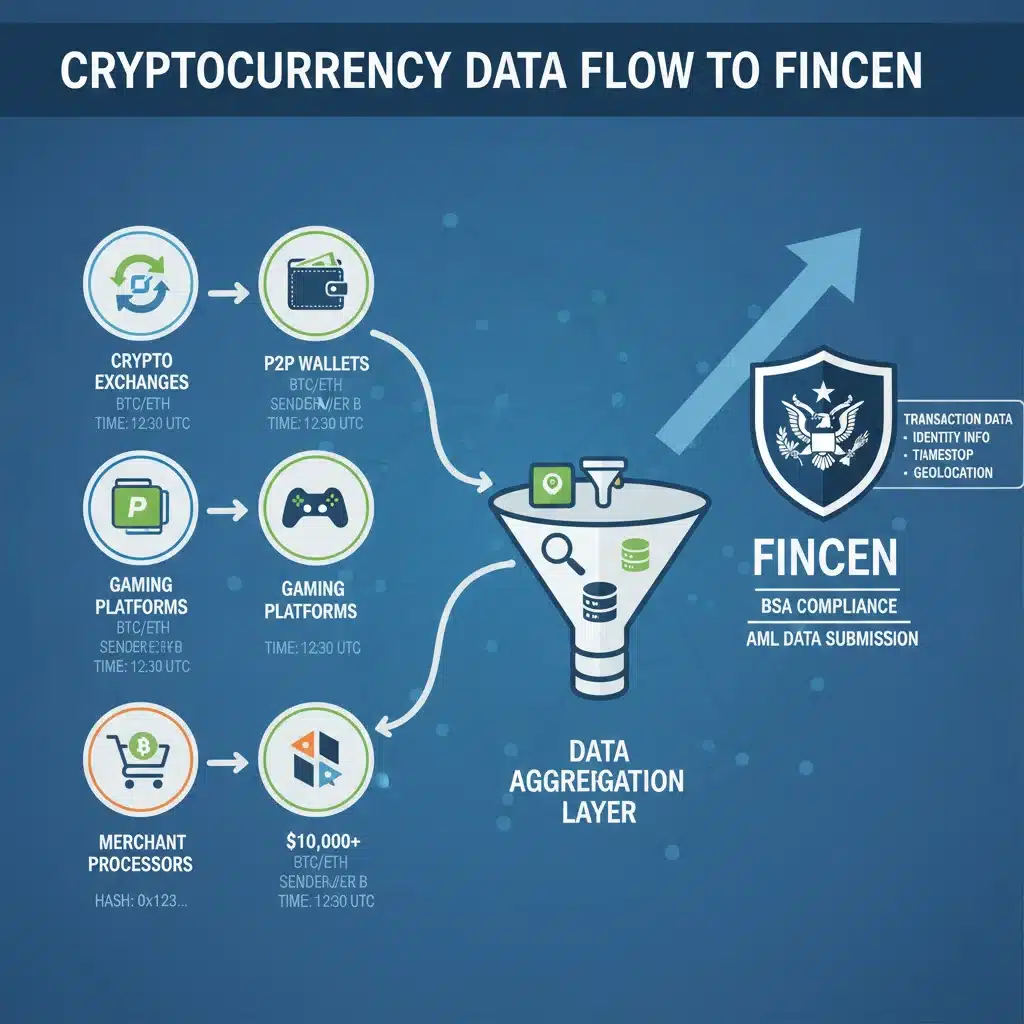

For US crypto businesses, FinCEN compliance primarily revolves around several key reporting mechanisms designed to provide transparency into financial transactions and identify suspicious activities. Understanding these obligations is the first step towards effective preparation for the Q3 2026 deadlines.

1. Suspicious Activity Reports (SARs)

Perhaps the most critical reporting obligation, SARs are filed by financial institutions, including designated MSBs like many crypto businesses, when they detect suspicious activity that may involve money laundering, terrorist financing, or other illicit financial activities. The threshold for filing a SAR for virtual asset transactions is generally $5,000, though institutions are encouraged to file even for lower amounts if the activity appears suspicious. Key indicators of suspicious activity in the crypto space can include:

- Unusual transaction patterns (e.g., frequent, large-value transactions that deviate from a customer’s normal activity).

- Transactions involving sanctioned jurisdictions or entities.

- Attempts to obfuscate the source or destination of funds (e.g., using mixers/tumblers, multiple layers of transactions).

- Customer behavior indicative of money laundering (e.g., providing false identification, refusing to provide information).

- Transactions linked to known scams, hacks, or darknet markets.

The timely and accurate filing of SARs is crucial for law enforcement to track and disrupt illicit financial networks. The Q3 2026 deadlines will likely emphasize the quality and completeness of SAR filings related to virtual assets.

2. Currency Transaction Reports (CTRs)

While the name ‘Currency Transaction Report’ might suggest fiat currency, FinCEN has clarified that certain virtual asset transactions can trigger CTR requirements. Specifically, if a crypto business facilitates the exchange of virtual currency for fiat currency (or vice versa) in amounts exceeding $10,000 in a single day, or across multiple related transactions, a CTR must be filed. This applies to both inbound and outbound transactions. The challenge for crypto businesses often lies in accurately aggregating related transactions and ensuring robust tracking mechanisms are in place to identify these thresholds.

3. Reports of Foreign Bank and Financial Accounts (FBARs)

Though primarily associated with traditional financial accounts, the FBAR requirement can extend to virtual assets in certain circumstances. U.S. persons with a financial interest in, or signature authority over, one or more accounts located outside of the United States, if the aggregate value of those accounts exceeds $10,000 at any time during the calendar year, must file an FBAR. While FinCEN has not explicitly stated that virtual currency wallets held on foreign exchanges always constitute ‘accounts’ for FBAR purposes, the evolving interpretation suggests that entities holding significant virtual assets abroad should assess their FBAR obligations carefully. This area is particularly ripe for further clarification as Q3 2026 approaches.

4. Recordkeeping Requirements

Beyond reporting specific transactions, FinCEN imposes extensive recordkeeping requirements on crypto businesses. These include maintaining records of customer identification, transaction details, and communications related to suspicious activities. Adequate recordkeeping is not only a compliance obligation but also a foundational element for efficient reporting and for demonstrating adherence to AML programs during audits or examinations. The ability to retrieve and present comprehensive transaction data quickly will be critical for meeting FinCEN’s expectations.

Challenges Unique to FinCEN Crypto Reporting

While the principles of BSA/AML compliance are generally consistent across financial sectors, virtual assets present several unique challenges that crypto businesses must address when preparing for the Q3 2026 deadlines.

1. Pseudonymity and Decentralization

The pseudonymous nature of many blockchain transactions makes it difficult to identify the true parties involved without sophisticated analytics and enhanced due diligence. Decentralized finance (DeFi) protocols further complicate matters, as they operate without traditional intermediaries, making it challenging to assign reporting responsibility. FinCEN’s guidance has attempted to bring certain aspects of DeFi under its purview, but the technical and operational complexities remain significant.

2. Global Nature of Transactions

Cryptocurrency transactions are inherently global, often crossing multiple jurisdictions in seconds. This poses challenges for determining which regulatory framework applies, especially when dealing with international counterparties or platforms. US crypto businesses must ensure their compliance programs account for both domestic and international regulatory expectations.

3. Rapid Technological Evolution

The crypto space is characterized by rapid innovation, with new tokens, protocols, and transaction methods emerging constantly. Keeping compliance systems updated to account for these technological advancements – from new privacy coins to novel staking mechanisms – is a continuous challenge that requires significant investment in technology and expertise.

4. Data Volume and Complexity

Blockchain networks generate massive volumes of transaction data. Extracting, analyzing, and structuring this data in a format suitable for FinCEN reporting requires specialized tools and skilled personnel. The complexity of different blockchain structures and transaction types further adds to this challenge.

5. Evolving Regulatory Interpretations

Although FinCEN has issued significant guidance, interpretations of existing regulations continue to evolve, particularly as new virtual asset products and services emerge. Staying abreast of these developments and adapting compliance programs accordingly is a constant endeavor.

Strategic Preparation for Q3 2026 FinCEN Reporting Deadlines

Given the complexities and the approaching Q3 2026 FinCEN reporting deadlines, a strategic and multi-faceted approach to preparation is essential. Here’s a roadmap for US crypto businesses:

1. Review and Update Your AML/BSA Program

Your existing AML/BSA program is the cornerstone of your compliance efforts. It must be specifically tailored to the unique risks presented by your virtual asset activities. Key areas for review and update include:

- Risk Assessment: Conduct a thorough, up-to-date risk assessment that identifies and evaluates the money laundering and terrorist financing risks specific to your products, services, customers, and geographic locations.

- Customer Identification Program (CIP) & Customer Due Diligence (CDD): Enhance your CIP and CDD procedures to effectively identify and verify the identity of your customers, including beneficial owners. This may involve leveraging advanced identity verification technologies and conducting ongoing monitoring.

- Enhanced Due Diligence (EDD): Implement robust EDD procedures for high-risk customers, politically exposed persons (PEPs), and transactions involving higher-risk jurisdictions or virtual assets.

- Monitoring and Alerting Systems: Ensure your transaction monitoring systems are capable of detecting suspicious patterns in virtual asset transactions, including those related to mixers, darknet markets, and sanctioned addresses.

- Internal Controls: Establish strong internal controls to ensure compliance with all BSA requirements, including the proper segregation of duties and clear lines of responsibility.

2. Invest in Technology and Data Analytics

Manual processes are simply not sufficient for effective FinCEN Crypto Reporting. Crypto businesses must invest in and leverage advanced technology solutions:

- Blockchain Analytics Tools: Implement tools that can trace transactions across different blockchains, identify suspicious addresses, and provide insights into the source and destination of funds.

- Automated Transaction Monitoring: Deploy systems that can automatically flag transactions that meet predefined suspicious activity criteria, reducing the burden on manual review and ensuring timely detection.

- Reporting Software: Utilize specialized software designed for FinCEN reporting (SARs, CTRs) that can integrate with your transaction data, streamline the filing process, and ensure accuracy and compliance with reporting formats.

- Data Management Systems: Develop robust data management systems capable of storing, organizing, and retrieving large volumes of virtual asset transaction data securely and efficiently, critical for recordkeeping and audit responses.

3. Staff Training and Expertise Development

Even the best technology is ineffective without knowledgeable personnel. Comprehensive training is crucial:

- Regular Training Programs: Implement regular and mandatory training programs for all relevant employees, covering FinCEN regulations, BSA/AML policies, and the specific risks associated with virtual assets.

- Specialized Compliance Team: Consider establishing or expanding a dedicated compliance team with expertise in both traditional financial regulations and the unique aspects of cryptocurrency.

- Staying Updated: Encourage continuous learning and professional development to keep staff updated on the latest regulatory changes, technological advancements, and emerging typologies of financial crime in the crypto space.

4. Establish Strong Governance and Oversight

Effective compliance requires strong leadership and oversight from the top:

- Designate a Compliance Officer: Appoint a qualified individual with sufficient authority and resources to oversee the AML program and FinCEN reporting efforts.

- Board and Senior Management Involvement: Ensure that the board of directors and senior management are actively involved in and committed to the compliance program, demonstrating a ‘tone from the top’ that prioritizes regulatory adherence.

- Independent Audits: Conduct regular independent audits of your AML program to assess its effectiveness, identify weaknesses, and ensure continuous improvement. These audits should be performed by qualified internal or external parties.

5. Engage with Legal and Compliance Experts

The regulatory landscape is complex and constantly shifting. Partnering with legal counsel and compliance consultants specializing in virtual assets can provide invaluable support:

- Regulatory Interpretation: Obtain expert advice on interpreting FinCEN’s guidance and how it applies to your specific business model and product offerings.

- Policy Development: Engage experts to assist in developing or refining your AML policies and procedures to ensure they are robust and fully compliant.

- Pre-Audit Preparation: Utilize consultants to conduct mock audits and help prepare your business for potential FinCEN examinations.

The Consequences of Non-Compliance

The stakes for non-compliance with FinCEN regulations are incredibly high. The penalties can be severe and multifaceted, impacting a business’s financial health, operational capabilities, and reputation:

- Significant Fines: FinCEN has the authority to levy substantial civil money penalties for BSA violations, which can run into millions of dollars. In some cases, criminal penalties can also be pursued.

- Reputational Damage: A public enforcement action or compliance failure can severely damage a crypto business’s reputation, eroding customer trust and making it difficult to attract new users or partners.

- Operational Restrictions: Non-compliant businesses may face operational restrictions, including the inability to conduct certain transactions, engage with financial institutions, or even a complete cessation of operations.

- Loss of Licenses: For licensed MSBs, repeated or severe non-compliance can lead to the revocation of their operating licenses, effectively shutting down the business.

- Increased Scrutiny: Businesses with a history of compliance issues are likely to face ongoing and intensified scrutiny from regulators, leading to higher compliance costs and administrative burdens.

Given these potential consequences, the investment in robust compliance infrastructure and proactive preparation for the Q3 2026 FinCEN reporting deadlines is not an expense but a critical investment in the long-term sustainability and success of any US crypto business.

Looking Beyond Q3 2026: The Future of Crypto Regulation

While the immediate focus for US crypto businesses is on the Q3 2026 FinCEN reporting deadlines, it’s crucial to recognize that the regulatory landscape will continue to evolve. FinCEN, alongside other agencies like the SEC, CFTC, and IRS, is continuously assessing and adapting its approach to virtual assets. Future developments could include:

- Further Clarification on DeFi: Expect more specific guidance on how FinCEN’s rules apply to various decentralized finance protocols and the responsibilities of different participants within the DeFi ecosystem.

- International Harmonization: As global efforts to regulate crypto intensify (e.g., FATF recommendations), there may be increased pressure for greater harmonization of regulatory standards across jurisdictions.

- Emergence of New Technologies: The development of central bank digital currencies (CBDCs), new privacy-enhancing technologies, and novel blockchain applications will undoubtedly prompt further regulatory responses.

- Increased Enforcement: As the regulatory framework matures, it is highly probable that FinCEN and other agencies will increase their enforcement actions, signaling a zero-tolerance approach to non-compliance.

Therefore, US crypto businesses should adopt a forward-looking and agile approach to compliance, viewing the Q3 2026 deadlines not as a final destination but as a significant milestone in an ongoing journey of regulatory adherence and responsible innovation.

Conclusion

The Q3 2026 FinCEN reporting deadlines represent a critical juncture for US crypto businesses. The time for passive observation is over; proactive and comprehensive preparation is now a mandatory aspect of operating in the virtual asset space. By understanding FinCEN’s mandate, identifying key reporting obligations, addressing unique challenges, and implementing strategic preparation measures, businesses can not only meet their compliance responsibilities but also strengthen their operational resilience and build greater trust within the broader financial ecosystem.

The path to full compliance may seem daunting, but with the right strategy, technology, and expertise, it is entirely achievable. Embrace this opportunity to refine your compliance framework, demonstrate your commitment to combating financial crime, and position your business for sustainable growth in the evolving world of digital assets. The clock is ticking, and preparation starting today is your best defense against future challenges and your strongest asset for long-term success.